Is Buffet's Mantra of "Don't Lose Money" Misleading You?

Is Buffet's Mantra of "Don't Lose Money" Misleading You?

Why “Don't Lose Money” might be misunderstood and may be the reason why you end up losing money in the stock market.

Hello, StockStars!

Let me start with a statement.

Buffet’s wisdom isn’t just in his words but in the depths and hidden layers beneath them.

This piece will ignite some contrarian thinking and may shake up some common investment beliefs. We start slow and get up to high speed - hold tight.

Ready?

If you’re new here, a warm welcome from my side! If not, you know what to do.

I’m Michael and on a mission to make beating the stock market as easy for you as choosing your favorite ice cream.

Last year, I started on a wild journey to write an algorithm that does exactly that.

Read the full story here.

Here’s what you get:

How doubling your earnings against the risk-free terrain becomes possible.

How long will it take until you arrive safely in the profit zone?

Buffet’s rule #1: “Don’t lose money!” Why many might get it wrong and therefore ... lose money?

Recapping the Path So Far

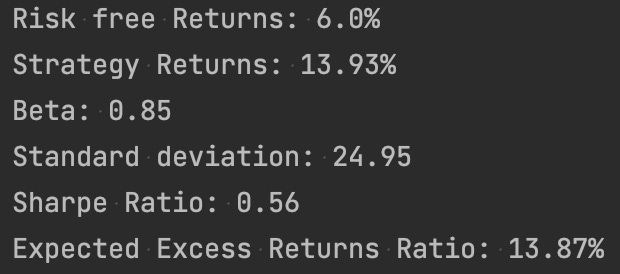

On our last date, I showed you my algorithm’s performance - a respectable 13.93% annual return. But as the ambitious tribe we are, we’re chasing more on our vision board.

Let’s dive into the strides and how we already got closer to the 20% mark.

Off into the algorithmic pot

I’ve chiseled away potential enhancements and, voilà, ten improvements later, we’re on a more profitable path. I won’t inundate you with the nitty-gritty and instead spotlight a few things.

Remember the “beta” talk last time?

A quick refresh: A beta above 1 shows higher volatility than our benchmark (in this case, Dow Jones). A beta below 1 shows lower volatility. Put simply, it’s the financial ups and downs.

The common belief?

A higher beta is riskier.

Risk vs Reward: The Age-old Conundrum

Stock market investments come with expectations of juicy returns. But with great returns, often comes greater risk. Isn’t it?

Let’s consider a hypothetical 6% return from a “risk-free” venture like a treasury bill. Sounds tempting, right?

Yet, when the Dow Jones averages a 7.26% return between 1998 and 2022, it’s hardly a party.

But a 16%+ return? Now that’s a reason to tango!

Decoding Risk

Prepare for a sprinkle of math (promise it’s a sprinkle).

Three numbers are crucial:

Standard Deviation: Think of it as an elastic band. The average return is the midpoint, and the deviation stretches it up or down. Look at it as the units of risk.

If you want to understand more. (Click here)

Sharpe Ratio: The Sharpe ratio, also known as the reward-to-variability ratio, measures the excess return of a strategy per unit of risk. It tells you the extra earnings for every 1% unit of the standard deviation over the risk-free option.

The higher the number, the more the Benjamins for you. If the Sharpe Ratio is negative – run away fast!!

A negative Sharpe ratio screams that not even the „risk-free“ money market return (in our case the 6%) has been outperformed. Thank god, ours is positive.

Return Over Risk-Free: This is the final result we are all interested in. How much more cash do you get into your account annually compared to the risk-free returns?

Our strategy’s evolution so far

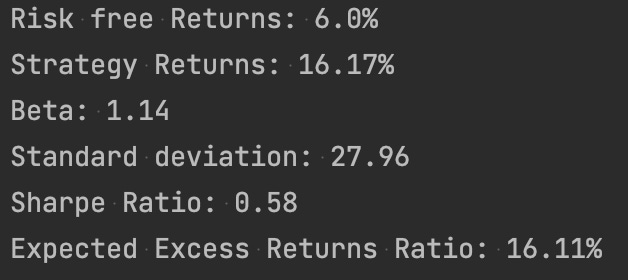

So let's look at the "ValueVantage 2.0" strategy from last time.

In our case, we multiply 24.95 by 0.56 and get 13.87% more money.

That’s good.

(If you don’t round the numbers you end up with 13.97%.)

Diving into the latest strategy update (the picture below), there’s an uptick in beta. In simple terms, when set against the Dow Jones, our updated strategy is experiencing more highs and lows.

Here’s the silver lining:

Both, the strategy returns and the Sharpe Ratio are on the rise. That’s pretty good since we are in the game of making money in the market.

The Waiting Game - How long does it take to become profitable?

You may wonder; how long do we have to wait before our strategy shines? The longest time period until this strategy really sparkles?

After the fifth year at the latest, the total return is always above our initial investment. From then on, we never look back.

$100.000 would have grown to over $2.2 million. Yes, there are still ups and downs, but after 25 years we have a staggering 500% more wealth compared to the risk-free route.

I told you, the strategy is simple, but not easy for some.

To recap

The idea is, that you only roll your money once a year. Holding out for five years for returns can be daunting. Many investors, tempted by the allure of quicker gains, jump ship, seeking the next golden strategy.

But think of investing not as a 100-meter dash but a decade-long marathon. It’s essential to invest funds you won’t immediately need.

Why?

Because the moment you’re financially pressed, your decisions morph - they become emotional, impulsive. Think back to the fervor of your first romance. And as we have already mentioned, emotions in investment are what? They’re the ultimate enemy.

Sounds so simple, and still – hard to execute for most investors.

Yes Michael, but what if we put in a stop loss to not lose money?

Glad you’ve asked.

Buffet’s Mantra Revisited

While the “Don’t lose money” mantra resonates with most, there’s a catch I think. If you hastily exit a declining stock, do you re-enter if it surges again?

Let’s take a deeper look at what this hasty exit-entry game can do with your gains.

At a cursory look, Warren’s advice seems rock solid: sell when stock prices dip to shield yourself from further losses. Roger that.

Makes total sense - on the surface.

But let’s play this scenario out. Suppose the stock price takes an upswing after you’ve sold.

The question then becomes, when do you jump back in? Factor in the x% dent in your savings because of your prior sale.

Now, re-entering the market at your exit point means buying fewer shares, thanks to the loss and additional transaction fees. If you decide to hold off until prices climb even higher for that added sense of security, you’re left with even fewer shares and fewer profits.

The result

Each trade chips away at your capital.

This is a losing battle. How am I so sure?

I’ve been down that road for the last two weeks. I’ve coded an aggressive selling strategy that activates at a 5% drop, aiming to stop any financial bleeding as soon as possible.

I tried re-entering the market at various points with the residual funds. Nope.

Multiple re-entries? Nope. Same outcome each time. It gets overwhelming, emotions explode, and you end up losing money.

Your overall performance takes a significant hit compared to just... standing still and doing nothing.

That’s where the quant approach shines - devoid of human emotions and biases, it offers a clear, rational pathway - if you trust in it.

The less you do, the better it is for your performance. Yes, stocks can plummet, but many rebound.

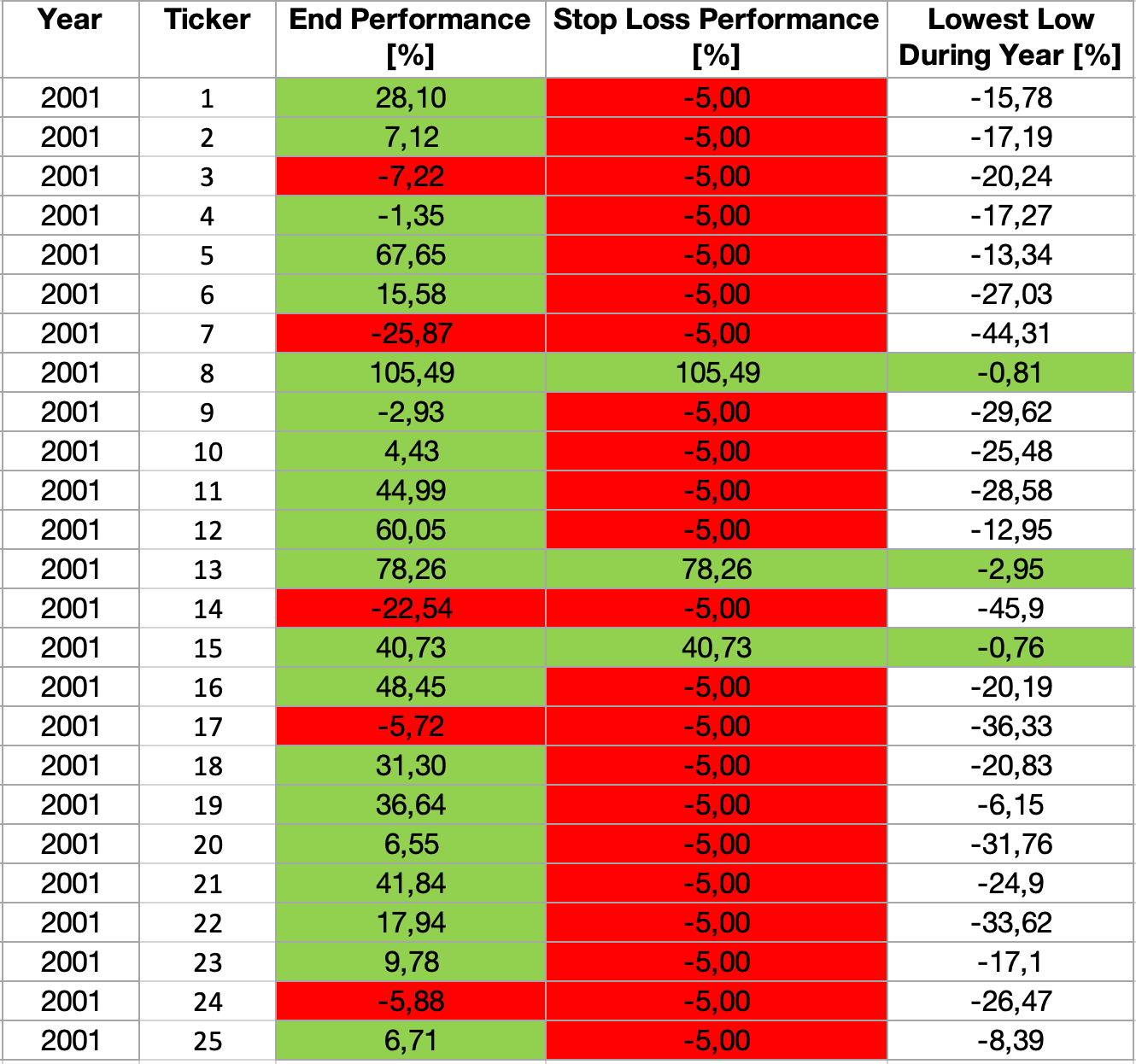

Look at the table below.

If we had exited at 5% stop-loss, look how many stocks came back after they fell below the 5% stop-loss and even lower.

An enormous difference

My algorithm picked 25 stocks for 2001.

The “End Performance” column is how the stocks actually performed in 2001.

The “Stop Loss Performance” column is how the performance would have looked like because a stop-loss of 5% was triggered by the last column.

The “Lowest Low During Year” column shows how far it went down during that year.

This is what reality in 2001 looked like for the 25 stocks.

(I did the same for other years with similar results.)

And that missed profit results from a rigid stop-loss approach that a lot interpret as “Don’t lose money”.

The stop-loss test result surprised me a lot, because it’s so counterintuitive, especially when I told you in another article, that you should use a stop-loss.

I will explain what changed my mind in a minute.

First another perspective

Yes, if you are not in the market, you can’t lose money and at the same time, you can’t make money either. That’s how this game works.

Pro investors like Warren Buffet know, that losing is part of the game. They lost as well. They also know you only need to win more than 50% of the time to make money.

Out of 25 years ValueVantage 2.0 won 72% of the time. Let that sink in.

Reality check

Before we close, I would like to add a thought, and it is sobering to say.

In the digital age, algorithms might just be the new wizards of Wall Street.

I recognize the countless dedicated individual stock analysts putting in manual work, sticking to what has always worked for them.

That method served me well for years, but it's like playing in another league.

But the real question is: How sustainable is that?

The golden opportunities to get prime stock deals and secure solid returns are narrowing rapidly. It’s an uphill battle against a machine (algorithms) that is designed for victory.

I hope I didn't come across too bluntly, but after pouring countless hours into this project, that's the stark truth I've uncovered. It was a revelation that really caught me off guard. It was like the moment of clarity one experiences when one sheds one's childish naiveté, and left me both stunned and speechless.

While the world of investing constantly shifts, it's not just about the returns. It's about adapting, understanding, and finding our own path in a landscape that's always evolving. Navigating alongside seasoned players can be a valuable learning experience. Remember, every step we take here together is a step forward together.

Conclusion

Let’s finish and let me explain what changed my mind.

Here’s the thing: the algorithm is discerning, selecting companies with sound backgrounds. It shoulders a massive burden for us.

The likelihood of these stocks bouncing back is higher than with a stock analysis that integrates earnings forecasts based on best guesses.

No one knows the future - and no expert does either.

My algorithm integrates a three-step strategy

On a high level.

A value strategy to identify “good” businesses.

A growth strategy to validate their values.

And a price momentum strategy that spots if the market has already caught on to a business’s worth, reflected in a rising stock price.

The rests are math and statistics.

The likelihood that something changes is also there, but I only lean on hard fundamental facts in my research, not on guesses aka forecasts.

All of this happens in near real-time, with almost 9,000 stocks being plowed through.

Find me a human who can replicate that.

It’s a tall order, and that’s exactly why investment firms charge a hefty sum for their algorithms that outperform the market.

They don’t play.

They are only in the market for one reason.

They want to make money.

Behind the Scenes

Progress:

My second vacation in Croatia was wonderful. I hope you’ve also soaked up the summer sun and recharged for the remaining year ahead!

The algorithm project name “ValueVantage 2.0” has further improved. I changed lots of code to get from 13.93% to 16% and tested a lot to gain more understanding.

I also changed the landing page on TheValueVantage.com

Plans:

The 20% return is our next goal.

A sliding window for reviewing the algorithm throughout the year,

followed by the reduction of beta (in the near future).

Where’s my head?

I love the progress in the last couple of weeks with a lot of aha moments.

Remember that my wife told me I need - a hobby. I’ve done some research on the private pilot license (PPA) topic. It’s doable. The only question is when, since it is a big time commitment and this project here has priority. I will start reading a book about flight theory and decide on it later.

Push that heart button, or your stocks might just show you a 'no-growth' face.

That’s it for today.

Until we meet again, au revoir StockStars!

Michael

If you think somebody should read this, be a good human, share it, and make them happy

Disclaimer:

The information in this article is my personal opinion. I’m not a certified investment professional. It is not consulting, nor does it constitute investment recommendations.

I do my research carefully and follow my personal investment strategy.

The stock market is a complex building with its own rules. There are no rules set in stone, like the rules of physics.

Therefore, use the contents of this newsletter at your own risk and do your own research as well. Investing in the stock market can lead to a total loss of the capital invested.

This first quote makes me think ...